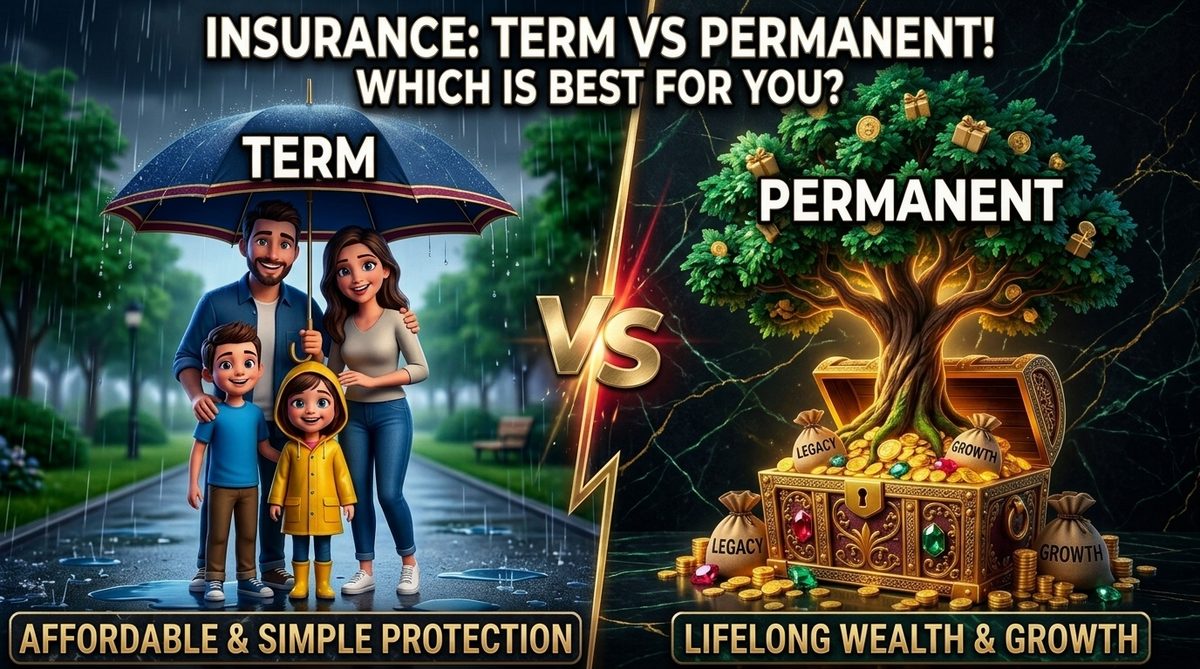

The same product, two ways

The default build puts your entire premium into base insurance. It maximizes the death benefit, and it maximizes the agent's commission, and your cash value in year one is roughly zero. Ten years in, you're still waiting for the policy to catch up to what you've paid. When someone says whole life is a rip-off, this is the policy they met.

The high cash value build flips the proportions. A small base premium, a large flow of paid-up additions, and a term rider holding the death benefit up while the cash value catches up. PUAs are small chunks of fully-paid-for insurance that go to work immediately, the branches on the tree. They also pay the agent little, sometimes nothing, which tells you something useful: good design pays the agent less. The shape is the point, and the shape is a design choice.

Not all whole life policies are created equal. Same premium, opposite outcomes, and the label on the folder looks identical.